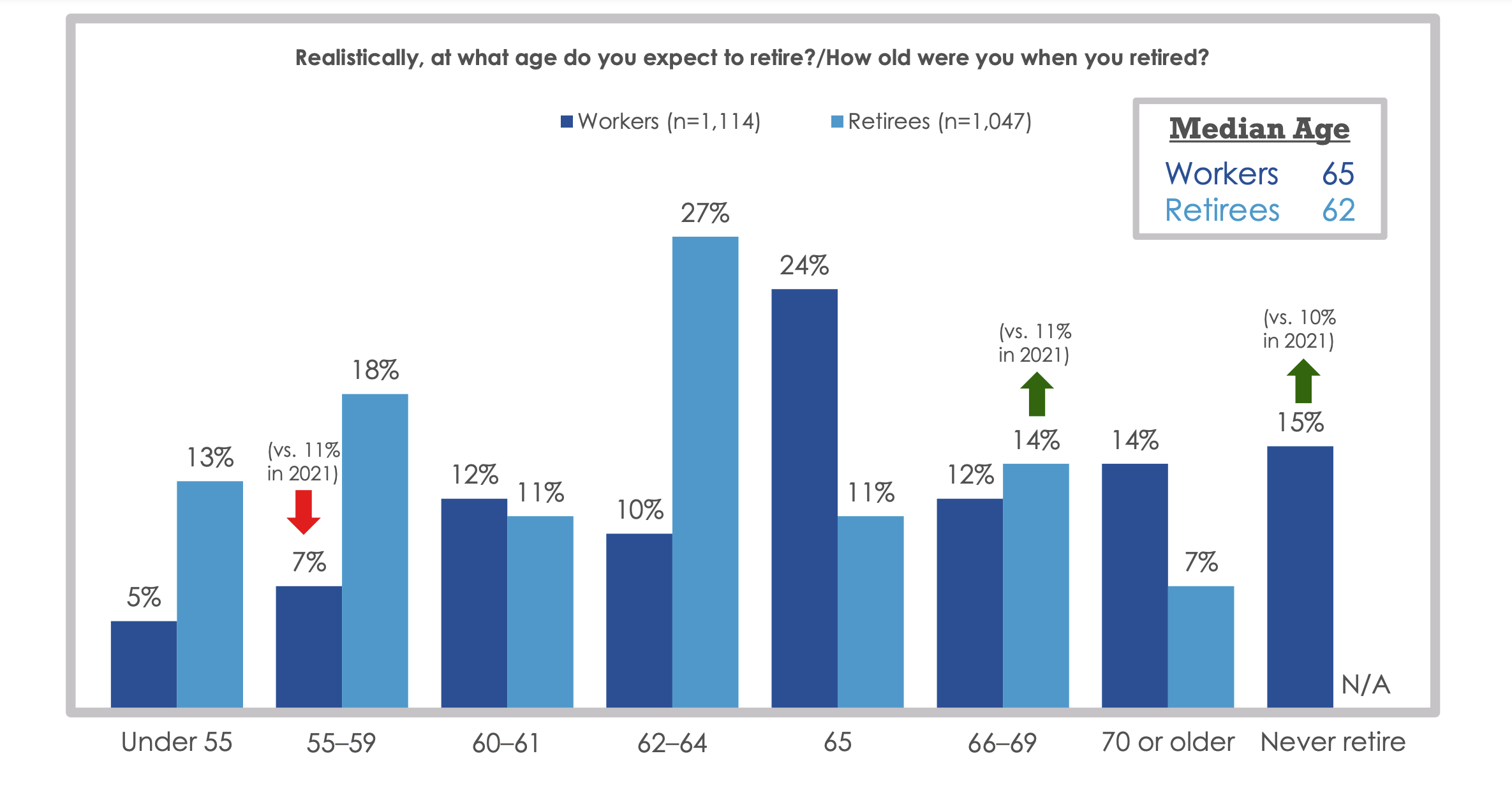

Most people assume they can work longer but end up retiring earlier. There could be multiple reasons, including health and unforeseen circumstances like COVID. It is wise to delay our gratification and save and invest while we are young and working. In a recent survey by EBRI, only 10 percent of the workers planned to retire at 62-64, but 27% of workers quit, straining the retirement funds.

Suppose a 60-year-old worker begins collecting Social Security at age 62; the monthly benefit will be $2,129. At full retirement age, or at age 67, the social security amount will increase by 43% to $3,042 and $3,772 a month if social security was drawn at age 70, an increase of 77% more than what the benefits at age 62.

Health is a significant factor in determining when to start collecting social security. If the 60-year-old is currently in poor health, delaying Social Security might not be the best option. The bigger monthly benefit is offset by the reduced number of years workers are projected to live.